Given the events of the last few weeks (North Korea, Charlottesville, etc.) as well as seasonality, the U.S. equity markets have moved into a correction phase. Over the last few months, the market has experienced several shallow 2%+ corrections and has snapped back within a few days with a new high. This action is very reminiscent of the bull market from 1994 to March of 2000, with the exception of the 1998 Russian Ruble, Asian, and LTCM liquidity crises, which, collectively, produced a sharp 20% drop in one month. The U.S. Fed dropped rates quickly and the market recovered. From that correction low to the end of the bull market in March of 2000, the Dow doubled and the U.S. GDP peaked at 7%. The Fed continued to push rates up and eventually pricked the dot-com bubble.

I believe the S&P 500 is most vulnerable to a drawdown as it is supported mainly by six tech stocks: Facebook, Apple, Amazon, Microsoft, Netflix, and Google.

Although I do not believe the bull market is over, a few items have come to light from my research that are concerning:

- More stocks are making new 52-week lows than new 52-week highs.

- For the first time since the mid-2000s, I’m starting to notice equities of companies that miss their earnings and revenue estimates get punished more severely than equities of companies being rewarded on the upside for exceeding their estimates. This suggests U.S. stocks are fully valued and priced for perfection.

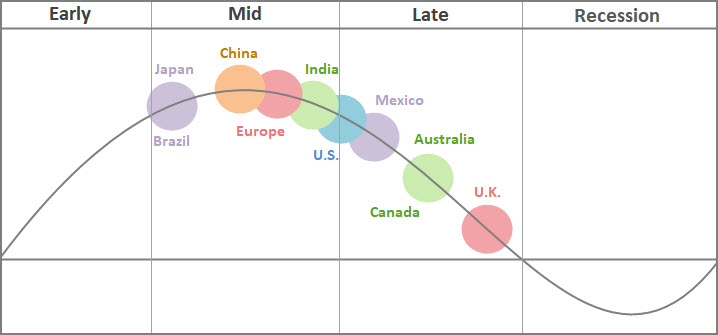

- The 8-year U.S. expansion is approaching “late cycle”. Japan & Brazil are early mid-cycle. China and Europe are mid-cycle. Australia, Canada, and the UK are deep into late cycle of their respective recoveries.

Source: Fidelity Investments (for illustrative purposes only)

- Real U.S. GDP y/y as of Q2 = 2.1%, which is the highest in 6 quarters. Euro area = 2.1% strongest since 2010. Japan 2.0% highest in 7 quarters. Interest rates in Japan & the EU are firmly planted at 0.0% where in the U.S. they are 1.25% and on their way up, but very gradual. I see a 50% chance of a rate hike at the September meeting.

- European stocks vs. the U.S. are the cheapest in 14 years. Japan/Asia ex-China the cheapest in 10 years.

- I believe the U.S. stock markets HAD priced in a successful passing of corporate & personal tax reform. Over the last few weeks public and corporate America has started to question the probability of that legislation being passed. Therefore the current correction/consolidation of U.S. markets may represent the repricing of that new probability.

- While a post correction rebound to new highs is possible, U.S. centric-economic concerns are starting to show. Bull markets usually end with the Fed pushing rates up to squash inflation and by doing so squash businesses as well. The result: an economic contraction/recession. We are not there yet. Possibly late 2018 or 1st half of 2019.

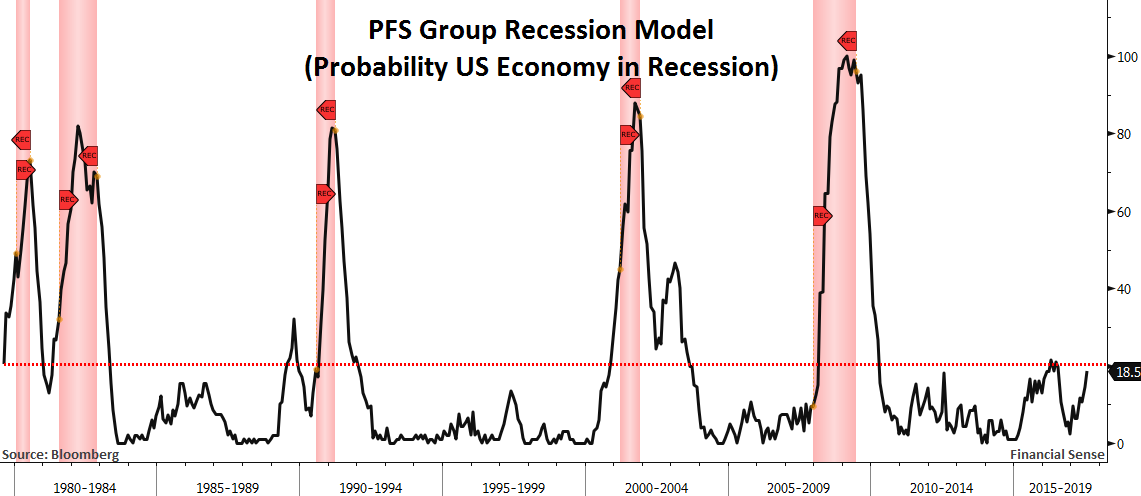

Source: PFS Group, Bloomberg

- The major world economies are now growing in sync. This is a byproduct of low interest rates from central banks around the world. In July of this year, the International Monetary Fund (IMF) forecasted global growth would come in at 3.5% for 2017 and 3.6% for 2018.

- Economic growth in the 19 nation Eurozone was greater than the U.S. in the first quarter and maintaining momentum for the second. EU unemployment has declined to a 9-year low.

It is my opinion that U.S.-based investors may want to consider a 25% equity allocation to international and 5% of that to the emerging markets.

Please contact Rob Bernard @ PFS Group @ 858-487-3939 or toll free @ 888-486-3939 with additional questions.