Originally published at The Boock Report.

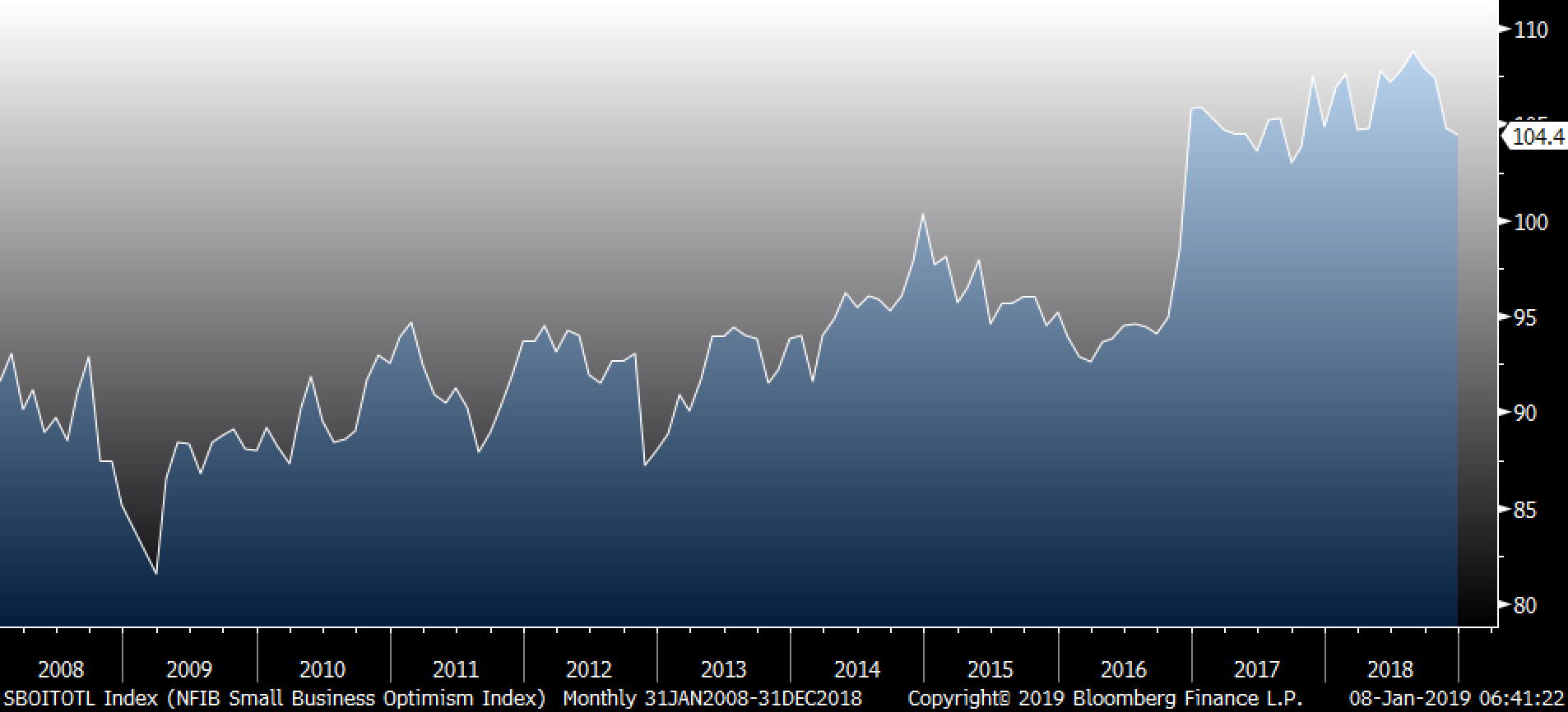

The December NFIB small business optimism index did slip by .4 points to 104.4. That is the fourth straight month of declines that took the index down by a total of 4.4 points and it now sits at the lowest level since October 2017. Some key components notably softened.

Capital spending plans fell four points to 25 percent, the lowest since November 2016, the month of the election and thus we've now given back all of the accelerated depreciation tax incentive enthusiasm. Debt deleveraging the new focus with one's cash flow? Those that Expect a Better Economy dropped by six points to 16 percent, the least since November 2016 (there goes all the corporate tax cut optimism). Those that Expect Higher Sales was down by one point to 23 percent and that's an eight-month low. Those that said it's a Good Time to Expand fell five points to the weakest since October 2017. What does this mean for Earnings Expectations? This component fell three points to -7.0 percent, the lowest in one year. Plans to Increase Inventories did rise six points but off the lowest level since April last month.

With respect to the labor market components, Plans to Hire did rise one point to 23 percent and that is smack on with the six-month average but the problem remains finding people that are qualified. Positions Not Able to Fill rose five points to the most on record. Compensation plans both current and future were little changed. Higher selling prices rose one point to match the highest level since May.

The NFIB is attributing the weakness in some notable categories to the difficulty in finding workers. I'm sure it is some of that but likely also reflecting softness in some key areas of the economy such as housing, manufacturing, exports, a flat lining in auto sales and the burden of tariffs for some (particularly the American farmer). I have to believe the weakness in the stock market has also impacted confidence because the NFIB spent part of its press release talking about the Fed and the stock market. "Since 2008, the S&P stock index has risen 110 percent, but U.S. output, measured by GDP, has increased only 25 percent over the same period. The growth in output owned by each share has lagged far behind the share price. So, as interest rates rise, bonds provide an attractive alternative to owning stocks and stock prices will weaken as investment money shifts to bonds."

NFIB Small Optimism Index

The German economy contracted in the third quarter from the second quarter and many attributed it to the issues with new auto emission rules which delayed the shipments of product. Well, that German weakness continued into the fourth quarter. We saw weakness in yesterday's November factory orders number and today industrial production was poor, falling 1.9 percent month over month, well worse than the forecast of up .3 percent. Also, October was revised down by .3. The Economic Ministry is blaming issues still related to auto's and the long weekends surrounding the holidays. Maybe some of the weakness was due to this but then we also got more data out of Europe.

The December Eurozone economic confidence index fell to 107.3 from 109.5. That's one point below expectations and is at the weakest level since December 2016. It's down eight points from where it sat at the end of 2017 when 'synchronized global growth' was the Davos mantra. The components covering manufacturing, services, the consumer and construction all fell month over month. Retail sales is the only one that rose and all it did was go to zero from -.5.

Maybe saying something about the dollar and the lack of Fed support now on rates, the euro is little changed notwithstanding the disappointing economic data out of Europe.

Moving to Asia, the consumer confidence index in Japan in December fell just .2 points but at 42.7, that's the weakest since November 2016. The Japanese economy has been so inconsistent during the reign of Abenomics and what exactly will be the Bank of Japan’s response when the next recession comes? Buy more bonds and stocks?

Bottom line to all this economic news today, buckle up for earnings season beginning in earnest next week. We will see some more Nike's but for sure more FDX, Apple's and Samsung's (blamed memory chips mostly overnight).

For daily macroeconomic analysis and asset class positioning, visit boockreport.com