Summary

- Investment Climate is moving sideways.

- Data does not indicate a cause for optimism.

- I will continue to be conservative through the end of the year.

Introduction

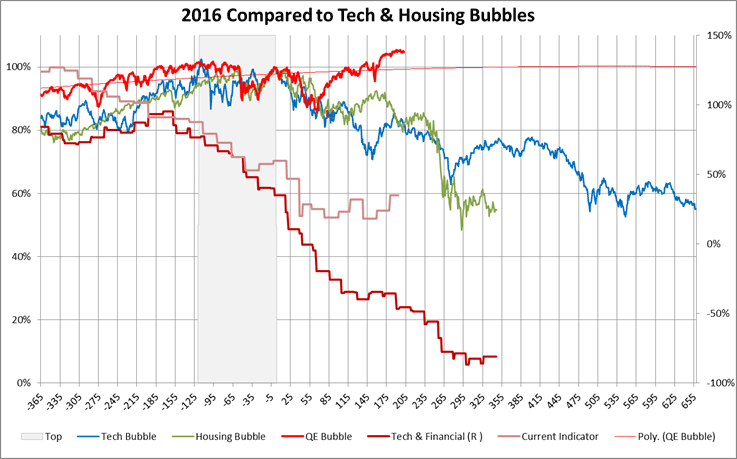

Of the monthly data that I track, 46% are trending negative compared to 62% last month. Of the quarterly data, 67% are trending worse. The chart below shows my Investment Indicator for the average of the Technology and Financial corrections (dark red line) and the current Indicator (light red). The Investment Climate was trending along the same path as it did during the previous two corrections until about April when it started flattening. The Wilshire 5000 (bright red) began increasing as the indicator stopped declining. The indicator took a breather the second quarter since its year-long decline. I am not convinced that it is improving or will continue its descent after the election.

Review of Data

The Economic Forecasting Survey by The Wall Street Journal has the probability of a recession occurring in the next 12 months at 21%, while JP Morgan put the odds at 37% in July.The Recession Indicator that I built from 15 indicators to lead the GDP Based Recession Indicator is shown below and it currently estimates a 40% probability of a recession starting over the next 12 months. I use the Recession Indicator as one of the 29 main indicators in the Investment Model.

Last month I referenced Doug Short’s article (see Visualizing GDP: An Inside Look at the Q2 Advance Estimate) that describes the second quarter GDP which was impacted by strong personal consumption spending and weak private investment (inventories). Since then, Lance Roberts wrote, “…the majority of American consumers have likely reached the limits of their ability to consume.” (See 3 Things: The Economic Fabric And Rising Recession Risks)

The following figure visualizes many of the main indicators that I use. The predominant trends are flat or downward.

The next chart shows how the main indicators compare to the previous two recessions. Some deterioration (blue) can be seen.

Indicator Highlights

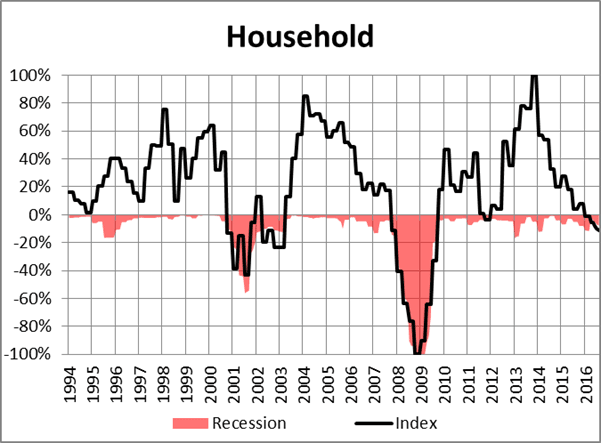

Below is my Household Indicator. It is a composite of year-over-year changes in Household Net Worth and Net Worth to Disposable Income. Growth in net worth has slowed which ultimately should have a negative impact on future spending since people are not seeing much growth in savings.

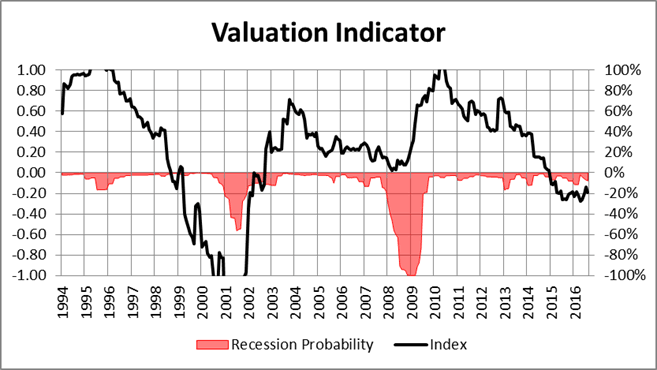

My valuation indicator is a composite of Capitalization/Gross Domestic Product, Tobin Q, Price to Earnings Ratio, and Cyclically Adjusted Price to Earnings. High valuations limit upside potential and according to some prominent investors will lead to low or negative returns over the next 7 to 10 years.

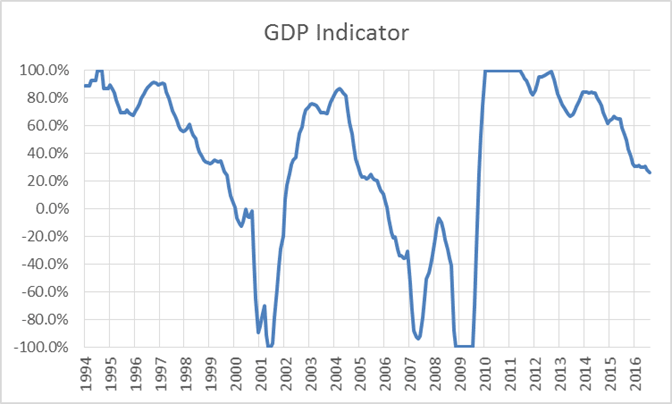

The GDP Indicator is a composite of the gap in GDP versus Potential GDP and growth in Real GDP supplemented by the Atlanta Fed GDP Now. GDP year-over-year growth has been less than 2% for several quarters. We are in a slow growth period that may last for many years.

The Leading Indicator shown below is a composite of State Leading Indicators, Chicago National Activity Index, Philadelphia Fed US Leading Indicator, and the Conference Board Leading Indicator. It is fairly neutral but declining.

My Risk Indicator is a composite of Financial Conditions, ST Louis and Kansas City Financial Stress, Volatility and Economic Policy Uncertainty. Financial Risk has been decreasing since the earlier in the year.

Below is the Corporate Indicator which is a composite of 7 sub-indexes. Corporate Profits, Disposable Income and Business Sales are the most negative of the sub-indexes. From Factset, “The second quarter marked the first time the index has recorded five consecutive quarters of year-over-year declines in earnings since Q3 2008 through Q3 2009.” “Less bad” is a good description for the corporate health.

The Income Indicator is a composite of Real Personal Income Excluding Transfer Receipts, Compensation of Employees and Real Disposable Income. Slower growth in income is likely to impact future spending.

The Spending Indicator is a composite of Real Retail Sales, Real Personal Consumption Expenditures, and Chicago Fed National Activity Index: Personal Consumption. It also shows some weakness.

Investment Model

My Investment Model was described in my first article on Seeking Alpha (see Using Economic Indicators to Evaluate the Investment Environment). The Investment Model is near my minimum level of allocation (15%) for stocks. It can be seen that the main composite index (dashed blue line) has stopped falling rapidly as it did prior to the last two recessions and in now moving sideways. The dark blue line is the stock market allocation index constrained by minimum and maximum stock market allocation. The underlying index began declining in Q3 of 2014 and I began reducing my allocation to stocks in Q2 of 2015. I use the Investment Model as a Nowcast and not for forecasting, however, the trends are estimated and shown in the chart to the end of the year. The trends are for a flat to slightly improving investment environment. With the unusual Presidential Election and aging business cycle, I will remain cautious through the end of the year.

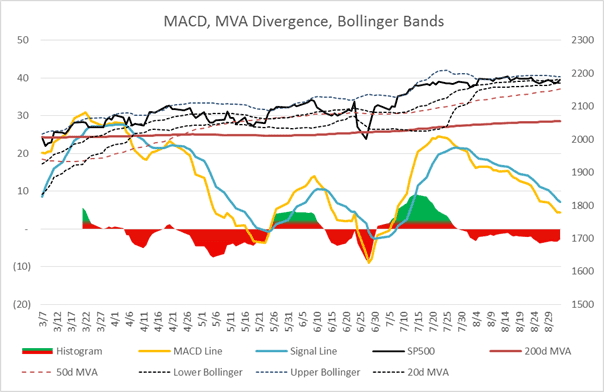

Short term, I believe there is a high potential for a seasonal dip in the stock market. The S&P500 has been moving sideways for over a month.

Validation

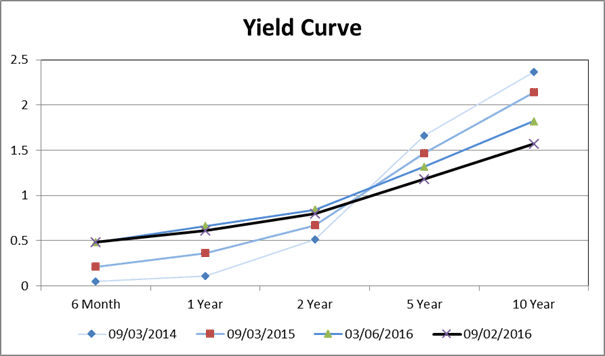

I like to validate the Investment Model with actual data as follows. The Yield Curve has flattened considerably during the past six months indicating that bond investors expect slower growth. Below I show the 10-year and 2-year treasury rates. When short-term rates are higher than long-term rates, the yield curve is said to be inverted.

Growth in National Activity, Consumer Spending (excluding food and energy) and Business Sales continue to slow. Industrial Production may have bottomed in the short term.

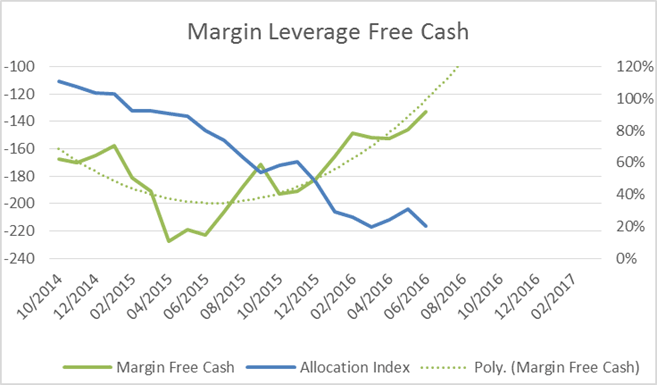

Margin Free Cash is starting to increase (be less leveraged). This is a sign investors may be becoming less bullish.

Banks continue to tighten lending standards. Investment is slowing.

Listening to the Pros

This is my favorite section. I save the articles that I read and highlight some of them before writing a new article. Here are a few of the ones that I found interesting.

Alex Barrow describes regulatory changes that will impact investing (see What the New SEC Money Market Fund Regulations Mean for the Financial System). He states, “These new rules basically say that prime and municipal money market funds (the funds invested in riskier assets than T-bills) will have to float their NAV’s.” I have begun leaving more “emergency funds” at the bank instead of mutual funds.

Previously in this article, I presented my GDP Indicator which incorporates the Atlanta Fed GDPNow. I have a casual observation that the GDPNow estimate has been starting estimates high at the start of the quarter and then declining by the end of the quarter, yet my indicator is declining. Marc Chandler describes how long-term estimates are based on population growth and productivity (see Bernanke's Advice: More Emphasis on Data, Less on Fed Guidance). Part of my GDP Indicator is based on the gap between GDP and Potential GDP. Marc concludes:

First, the downward revisions to the long term forecast imply that, on balance, Fed officials see the policy as less accommodative than previously thought, the labor markets are not as tight and price pressures more constrained. This speaks to a slower pace of normalization of US monetary policy. Second, Bernanke cautions Fedwatchers: They "should probably focus on incoming data and count a bit less on Fed policymakers for guidance."

Jeffrey P. Snider provides support for the Labor, Income and GDP indicators in a recent article (see Slowing And Even Contracting: Hours And Earnings). He states,”…a broad view of the labor market shows that what might have been limited (but forewarning) weakness in 2015 is spreading not abating such that even the labor market is showing signs of being broadly affected.”

The Munich-based Ifo Institute said that its World Economic Survey fell to its lowest level in over three years reversing the trends in confidence from the first quarter (see “World Economic Outlook Dips to 3-year low: Ifo”).

Conclusion

I have learned a lot from reading John Hussman’s articles. In Morton’s Fork, John describes my philosophy well (see Morton’s Fork):

“Whatever you do with your own portfolio, think carefully about the assumptions you are relying on, and whether those assumptions can be backed by evidence. Too many investors seem mesmerized by the idea that central banks have near magical powers, never fully defined, and never clearly articulated. The best advice I can offer is this: put your assumptions into words, and then take them to the data to make sure that what you believe is actually true.”

What do I believe to be true and shown in this article? The economy has been slowing since Q3 of 2014. The stock market is overvalued and profits declining. Many indicators are still declining. The latest data, on average, is neutral with half improving and half declining.

What do I believe without having sufficient data to prove it? I think the chances of the economy entering a recession in 2017 or 2018 is very high. Do a search on “Global Economic Risks 2017” and you are likely to make a list like the one below. I continue to be very conservative.

- Continuing impact from “Brexit” and possibly others (“Grexit”)

- Slow growth globally and in the US

- Currency wars

- High government debt

- Deflation or low inflation

- Excess capacity (and low investment)

- Low corporate profits

- Weaker growth in Asia including a possible hard landing in China

- Middle East conflict (Jihadi terrorism and population displacement)

- Unemployment in Europe

- Youth unemployment

- Stronger dollar and weaker US exports

- Asian military expansion

- Future oil shocks due to low current investment

- Trump Presidency (Economist)

- Impact of higher US interest rates on emerging markets

Disclaimer: I am not an economist, investment advisor nor investment professional. This material is for informational purposes only and should not be construed as investment, legal or tax advice. Investors should do their own research or seek the advice of investment professionals.