The stock market is down after reaching all-time highs again in March. That means it’s time to talk about black swans, dragon-kings, and other such ilk; never mind the winter is beginning to thaw and economic indicators are improving for the U.S. There will always be a reason why stocks are selling off. It’s our job as investors to decide if the crisis is minor and a buying opportunity or major and the catalyst for a major correction.

Let’s turn to the Chinese credit crunch and Dr. Copper, which has been the latest drum for bears to beat. Concerns have arisen that China’s economy is growing at a much slower pace than they've let on. This is based on the drop in winter manufacturing (PMIs), the recent trade deficit, a corporate bond default from Chaori Solar, a default of a coal-related high-yield trust that made bad investments, and the decline in copper prices on speculation that more commodity-collateralized debt will default.

China is restructuring from an investment-driven economy to a consumption-driven economy. Is it going to create a major crisis like the Asian Financial Crisis in 1997 and the European Sovereign Debt Crisis of 2010-12, or is it a minor one that will offer nothing more than a short correction and ultimately a buying opportunity? A China “hard landing” has been predicted by notable analysts for three years, but we have not seen the signs of a disruptive undertaking here. Nevertheless, let’s look at the facts and let the facts speak for themselves.

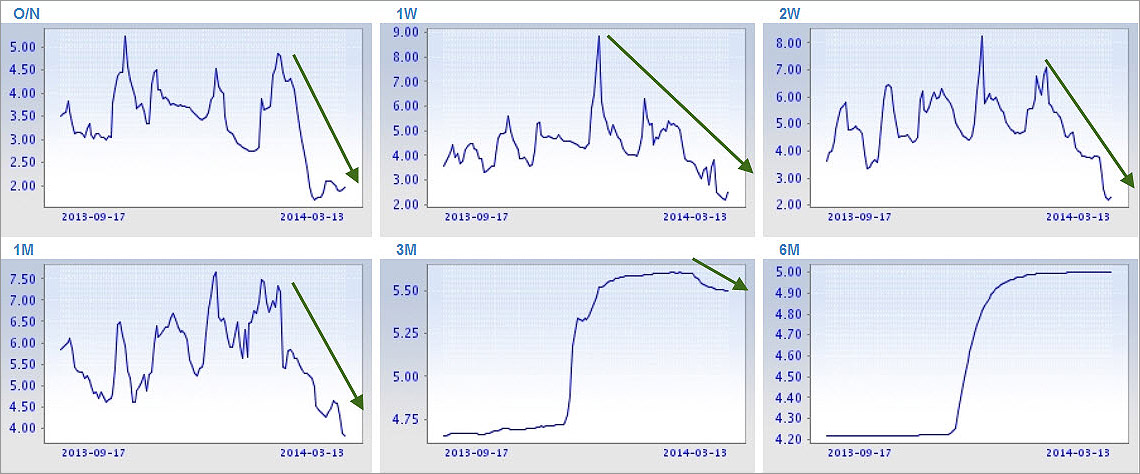

Falling Rates

Recent concerns started to arise in January with a rising Shanghai Interbank Offered Rate (SHIBOR) due to monthly bank reserve rebalances between banks and the People’s Bank of China (PBOC) and the availability of cash during the Spring Festival. If Chinese investors are as worried about credit as the media is, why are short-term rates falling instead of rising?

Source: Shibor

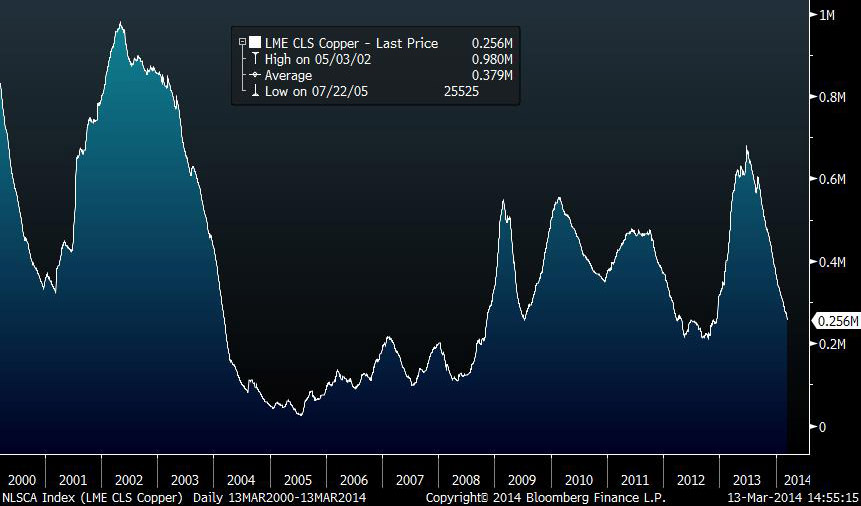

Reuters printed a story today that Chinese banks are cutting loans to its industrial sector, by as much as 20 percent. If China has said they’re going to move away from an investment-driven economy to a consumption-driven economy with less dependency on the U.S. and European markets, aren’t they merely doing what they said they would do? There’s no surprise. There will be a contraction in the investment economy while there’s growth in the consumption economy. The concern, however, is if in the process China slows down considerably, creating serious downside risk to emerging markets like Brazil, Canada, US, Australia, and others who ship materials to China. Are those concerns warranted? Yes. Can we put an indicator on China and global health? Yes. And while many don’t believe the metrics we get out of China, there are other ways to monitor global health besides just the price of copper, which is currently at long-term support.

JPM Global Manufacturing/Services PMI

Using the results of surveys from 11,000 purchasing executives in nearly 30 countries, Markit has compiled a composite that attempts to measure the activity of those countries that account for 86% of global GDP. These results aren’t filtered through labor bureau and bureaucracy. Currently, there was a lull in 2012 where the manufacturing index printed a contraction reading (below 50), but it has steadily been on the rise since then, and that has been continuing in 2014. The services PMI has not once dipped into contractionary territory since the global financial crisis of 2009 resided.

Source: Bloomberg

Baltic Dry Index

The Baltic Dry index measures the freight cost, weighted to the different sizes of ships, to carry dry bulk such as coal, iron, and grain across 23 shipping routes. It’s a good measure of supply versus demand, as prices should come down if demand drops or there’s a glut of ships, as was the case after 2008 when many were just used to park oil offshore.

Huge debt loads and falling commodity prices created a bubble in shipbuilders and operators over the years. Rates have begun to climb up once more since 2012 as demand has more equally matched supply and ship production has leveled off after the industry has had six years to consolidate. The Chinese PMI scare in January sent rates lower, but they’ve been steadily rising since then. Overall, it looks like a bottoming pattern to me that’s still developing these past three years.

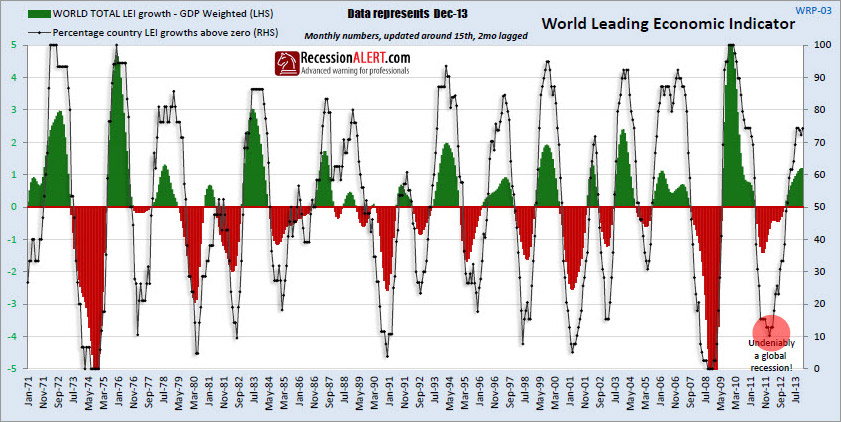

World LEIs

An independent research specialist, Dwaine van Vuuren, of RecessionAlert.com has done wonderful work on economic indicators. One of their great charts is the World Leading Economic Indicator which is GDP weighted with a 2-month lag. This chart, like the JPM Global PMI composite shows the world leaving the conditions of a global recession in 2012.

Source: Recession Alert

Their data shows that Chile, Israel, Mexico, Sweden, Brazil, China, India, Indoneisa, and South Africa are in a contraction while the rest of the world is expanding according to the leading economic indicators (LEI).

Summary

Commodities are rising and falling. The rising commodities are precious metals and softs due to weather in the US. Most of the economically-sensitive commodities like lead, copper, aluminum, and iron ore are down year to date. That’s bad for metal supplying economies and good for consumer-driven one's that buy goods and services. Falling metal prices, cheap credit, and a healthy consumer are some of the many reasons the auto and retail industry stocks have performed over the past two years.

It’s been written that China was going to kill the world economy for the last three years. So far, that hasn’t happened. Yes, copper is falling, and, yes, many companies use it as collateral, but banks required companies to hedge their exposure on the London Metals Exchange and that’s why we haven’t seen any panic selling other than in the copper iPath ETF (JJC) on Wednesday. Copper inventories have been drawn down across the globe over the past year and are nearly a third of what they were a year ago. Is it time to sell copper now? Probably not.

Source: Bloomberg