Originally posted at Briefing.com

There is no question that the U.S. economy is better today than it was when the Federal Reserve started down its path of quantitative easing in late 2008. What remains wide open for debate is just how much of the improvement is due to the Fed's QE program as opposed to normal cyclical factors at work.

Say what you will about the effectiveness of QE, or lack thereof, one thing that is undeniable is that its introduction succeeded in driving a major turning point in consumer and investor sentiment.

We draw your attention to this issue because it seems likely to us that the end of quantitative easing is nigh. Specifically, we think the Fed will announce the cessation of its asset purchases when it closes its October 28-29 FOMC meeting.

The Real Worry

The Federal Reserve, of course, has been tapering its monthly asset purchases throughout the year, cutting them in billion increments such that the pace of purchases has gone from billion per month in December 2013 to billion currently.

Under its current directive, the Fed is buying billion of agency MBS per month and billion of longer-dated Treasury securities.

With the Fed cutting its asset purchases this year on a regular basis and essentially telegraphing the end of that initiative, we found it somewhat bemusing to hear market pundits place a good bit of blame for the stock market's recent turmoil on the idea that the Fed's QE program is coming to an end.

[Hear: Rick Santelli: When the Music Is Playing, You Have to Get Up and Dance]

Really?

Neither the stock market nor the Treasury market freaked out with each successive taper this year. And when the S&P 500 rallied 6% between its August 7 low and its all-time high on September 19, there was scant attention to any impending misery that was going to result from the end of QE. On the contrary, the end of QE was heralded then by pundits as a sign of economic progress.

It was only when the stock market ran into a bout of sometimes inexplicable selling that the "end of QE" excuse was trotted out.

The First Dig

If the markets were worried about anything in recent months as it relates to monetary policy, it was the thought that the fed funds rate might be raised soon more so than it was the thought that QE would soon be ending.

After all, if the stock market wasn't unsettled when monthly asset purchases went to billion, billion, billion, billion, billion, and then billion, it doesn't make sense that it would be completely unnerved by the Fed pulling the plug on the final billion, especially when there have been pervasive doubts all along about QE's true impact on the real economy.

[Hear Also: Diane Coyle – GDP: A Brief But Affectionate History]

And the idea that there won't be a ready buyer of U.S. government debt after the Fed exits comes up short when taking into account that the yield on the 10-yr note came down from 3.02% at the end of 2013, when the Fed's asset purchases were billion per month, to as low as 1.85% earlier this month when the Fed's asset purchases were only billion per month.

We suspect the Fed will take those thoughts into consideration at the October FOMC meeting, along with the improvement in the labor market, as a basis for deciding to end its asset purchase program.

Something else to consider is that the Fed would be sending a startling economic message if it chose not to end its asset purchase program now.

[Read: The FOMC Takes Dollar Strength Into Account]

At this juncture, we think the Fed is anxious to get out of the asset purchase business and eager to start laying the foundation for a path to policy normalization. The first dig in that respect would be ending QE.

What It All Means

We began this week's column with the declaration that the U.S. economy is definitely better than it was when the Fed started the first wave of its asset purchases in late 2008. To be sure, it could still be doing a lot better than it is.

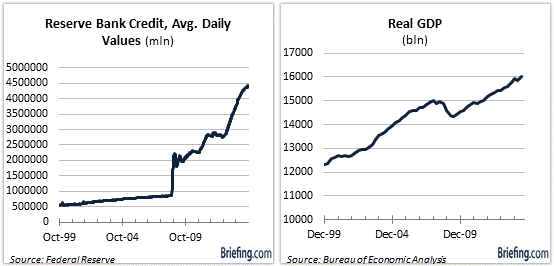

Its slow-growth trajectory six years after the start of what would be a trillion plus expansion of the Fed's balance sheet is a big reason why QE has been likened to pushing on a string and considered by many to have been a futile, and reckless, policy action.

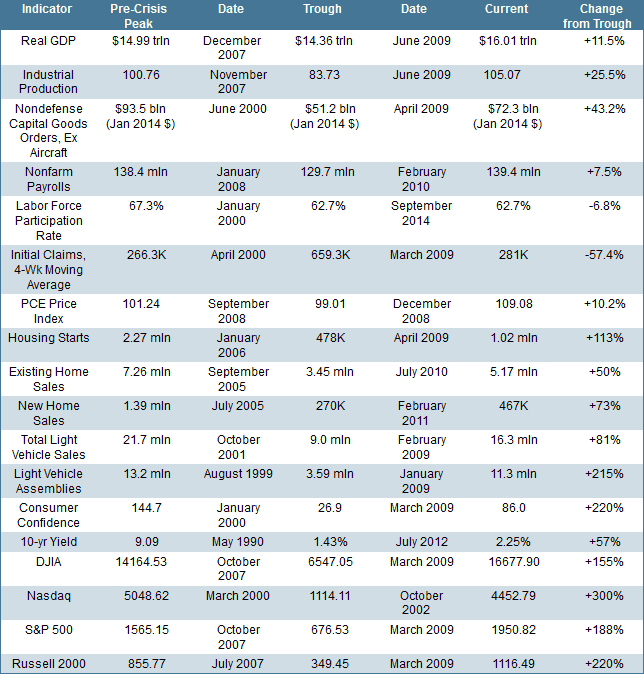

No matter what side of the QE debate you take, there is a range of available indicators that will shape the debate for decades to come about what impact QE really had. We present many of them below for consideration as the life of QE comes to an end. May it rest in peace.

Pre-Crisis Peak measured from 1989-2008