As a result of Troika-imposed austerity, Greece has a current account surplus that widened in September to over a billion euros.

This happened because demand for foreign goods collapsed in the wake of 27.3% overall unemployment and a shockingly high 57.9% youth unemployment.

The Coming Greek Default

In spite of a current account surplus, Greece's overall debt load is unsustainable.

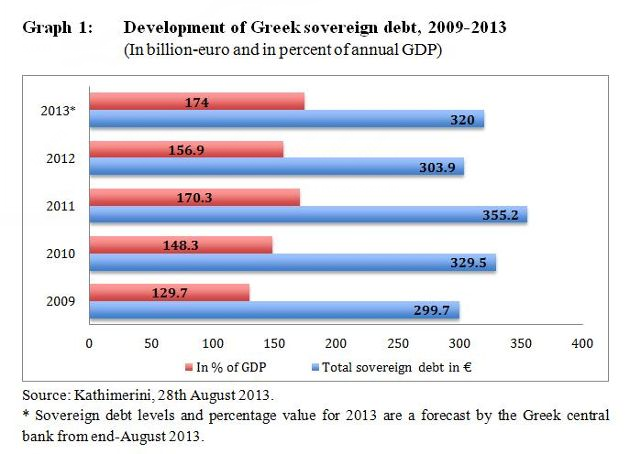

Here are a couple of key details: Greece has €320 billion in sovereign debt. Greece's debt-to-GDP ratio is 174%.

Recall that the Troika considered anything beyond 120% unsustainable. Also recall that Greek debt was restructured twice to meet those targets.

The pertinent question is not "How will Greece pay back €320 billion?" because it can't and won't. Rather, the pertinent question is "How will Greece NOT pay back €320 billion?"

Two Possibilities

- Default accompanied by an exit from the eurozone

- Debt relief from Germany and the rest of the eurozone

For political consumption purposes ahead of the last federal election, German chancellor Angela Merkel ruled out more aid to Greece. That blatant lie was probably enough to hold support for the eurosceptic AfD party below the 5% threshold to make German parliament. AfD failed by 0.2 percentage points.

Had Merkel admitted the truth, it's hard to say how many more votes AfD would have gotten, but I suspect far more than 0.2 percentage points.

With election lies out of the way, the corollary questions for Germany now are quite similar.

Questions for Germany

- Does Germany grant debt relief to Greece?

- If so, how?

- If not, when does Merkel admit she lied?

- If not, when does Merkel admit the consequences?

[Listen to: Martin Armstrong: The US Is the Beneficiary of Foreign Crises - Follow the Capital Flows]

Prisoner's Dilemma Game

This line of questioning creates a sort of Prisoner's Dilemma Game in which two individuals (in this case countries) might not cooperate, even if it appears that it is in their best interests to do so. Click on the link for prisoner's dilemma examples.

One way or another Germany is going to pay. Unless Germany forgives Greek debt, Greece is more likely than ever to default.

Why? Because Greece now has a current account surplus. It does not need to borrow money from foreign countries to finance its ongoing deficit (because there is no deficit).

Greece Strikes Back

The Financial Times reports Greece Strikes Back.

Ever since Greece entered its rescue programme in 2010, the relationship between Athens and its international lenders has been fundamentally unequal. Having lost access to the capital markets, the Greek government relied on the bailout funds to pay its bills.

With the public accounts edging closer to a primary surplus, the government feels it has a stronger hand to play. On Sunday lawmakers passed the 2014 budget without showing it to the IMF or the commission as demanded by EU rules. The vote sets the scene for a tense meeting when troika representatives return to Athens this month.

That Antonis Samaras, prime minister, feels the need to flex his muscles is understandable. His coalition’s parliamentary majority is now wafer-thin after defectors refused to vote for more austerity measures. Opposition parties, such as Syriza on the left and Golden Dawn on the right, are gaining strength thanks to their pledges to renegotiate the rescue deal or even abandon the single currency.

Yet Mr Samaras should be careful not to overplay his hand. —

Samaras Forced to Act Tough

The Financial Times warns Samaras. But what is Samaras to do? Note that Greek opposition leader looks to EU elections for mandate.

Alexis Tsipras, Greece’s far-left opposition leader, said the Greek government will no longer have a mandate to run the country if his Syriza party finishes first in May’s European parliament election.

He predicted that national elections would be held before the end of next year.

Mr Tsipras, who has vowed to scrap the country’s €172bn bailout agreement with international lenders, said anger in Greece has grown since last year’s national election when Syriza twice came close to becoming the country’s biggest party in parliament – falling just short of the centre-right New Democracy party of Antonis Samaras, now prime minister.

Unless Samaras talks tough, Syriza would likely win the next election and may do so anyway.

Tsipras would do one of the two major things that Greece needs to do: Tell the Troika "go to hell" then default. But Greece also needs a tremendous amount of structural reforms that none of the Greek political parties seems willing to address.

The key point is that as long as Greece runs a current account surplus, it can finance its way via taxation, without further Troika meddling.

Debt Relief or Debt Restructuring?

MacroPolis writer Jens Bastian asks Debt relief or debt restructuring for Greece?

The two economic adjustment programmes for Greece from 2010 and 2012 as well as the sovereign debt restructuring from April 2012 and the debt buyback initiative in December of the same year have had a significant impact on the debt profile of Greece as a sovereign debtor. Greece’s creditor structure in 2013 compared to the point of departure in 2010 hardly bears any resemblance.

Prior to the conclusion of the first economic adjustment programme more than 85 percent of Greece’s sovereign debt was held by private institutions. By contrast, following the twin debt restructuring and buyback exercise during 2012 over 80 percent of Greece’s sovereign debt now rests in the portfolio’s and budgets of the eurozone’s member states, the ECB’s and the IMF’s vaults as well as on the balance sheet of the European Stability Mechanism (ESM).

While in 2010 Greek sovereign debt was primarily held by German[2], French, Italian, Swiss and Japanese banks, the combination of two rescue programmes and debt restructuring have fundamentally altered the ownership structure of and accountability for the accumulated sovereign debt of Greece from the private to the official sector. Greece’s public creditors in Europe and Washington together now own roughly 84 percent of the country’s 320 billion euros in debt.

Who will blink first?

Has this secondary migration process tied the hands of Greece as a sovereign debtor and created a prisoner dilemma for the Troika of international creditors? Who will blink first in the OSI debate? Who will continue to defend his privileged senior creditor status and insist on 100 percent payback?

It took no less than European Commissioner for Employment Laszlo Andor of Hungary to get to the heart of the matter. While he argued that Greece did not need a third bailout, Andor was honest to say that what Athens really needed was to be given debt relief. -

“What Greece needs today is not a third bailout, but a proper reconstruction plan, which inevitably starts with a significant (emphasis added) debt relief and continues with programmes that bring fresh investments” (Kathimerini 2013).

Greek Sovereign Debt History

The ECB, EU, IMF, and politicians in various countries managed to transfer 80% of Greek sovereign debt from private hands into public hands. In essence, they bailed out banks and put taxpayers at risk.

Calculating taxpayer responsibility percentages of various countries is simple enough.

Eurozone Financial Stability Contribution Weights

The above table from European Financial Stability Facility

Three Key Facts

- Greek sovereign debt is €320 billion

- Public ownership of Greek debt (counting IMF and ECB) is 80%.

- 80% of €320 billion is €256 billion

Two Key Questions

- Who pays if Greece defaults?

- In what way?

Countries Responsible if Greece Defaults

Note that Greece can hardly be responsible for 2.81% (7.19 Billion) of its own debt so that amount needs to be distributed accordingly to make the percentages total 100%.

Otherwise, unless the IMF is willing to wave its debt, the numbers are approximately as shown.

Three More Questions

- Given Greece's current account surplus, who really has the upper hand here?

- Although Germany might be able to cough up €69 billion, where the hell is Spain going to get €30 billion?

- Where the hell is Italy going to get €45.7 billion?

Should Spain suffer enough at the Troika's hands to also reach a current account surplus, it will be in a similar position to Greece. In other words, the structure of the eurozone is such as to cause a cascade of disorderly breakups as soon as countries eliminate their deficits.

[Hear More: Simon Mikhailovich: Bonds Are Not A Safe Haven - Today's Population Hasn't Experienced a Bond Debacle]

Final Bonus Question

So Angela Merkel, when are you going to admit this setup, and what are you going to do about it?