Each year I make a pilgrimage to the Strategic Investment Conference in California to listen to, and report back to you, on the views from investment and economic luminaries such as Lacy Hunt, David Rosenberg, Kyle Bass, Jeff Gundlach, Niall Ferguson, Nouriel Roubini, Mohamed El-Erian, Gary Shilling and many others. There are two things that come from this annual trip – the first is the time to get away from my office and clear my head, and; secondly, to compare my thoughts, and analysis, against the view of my contemporaries to ensure that I don’t suffer from confirmation bias.

However, as I was sitting on the plane, I reviewed the recent economic data including the ADP employment report, the Chicago PMI, construction spending and the ISM manufacturing reports. The data, to say the least, was disappointing. These recent data releases continue to conform to, and confirm, my recent analysis that the “Hurricane Sandy” effect has likely run its course and that the economy is softening despite the Fed’s continued liquidity interventions. Let’s take a look at the data.

ADP Employment Report

The ADP employment report came in well below expectations for April showing just 119,000 jobs created. This down sharply from last month’s disappointing report which originally printed 158,000 jobs but was subsequently revised down to just 131,000. The estimate for the April ADP report was 155,000 new jobs. Oops.

The problem with the report is that the weakness seen is likely going to be reflected in the Bureau Of Labor Statistics (BLS) employment report on Friday. Currently, the average estimate for the official BLS employment situation report is 153,000 new jobs following a very disappointing 88,000 new jobs in March. Given the weakness in the ADP report it will not be surprising to see a weak employment report for April.

The chart below shows the net monthly change in jobs for both the ADP and the BLS reports. The trend in employment has been clearly slowing since last October.

As we discussed recently it is clear that employment has peaked for the current economic cycle. The chart below shows both the seasonally adjustment employment levels compared to a 12-month moving average of the non-seasonally adjusted data.

The importance here is that this peak in employment comes at a time when the Federal Reserve is engaged in massive non-traditional monetary actions in order to stimulate economic growth and increase employment. It appears, currently, that the effect of those monetary measures have reached the limits of their effectiveness.

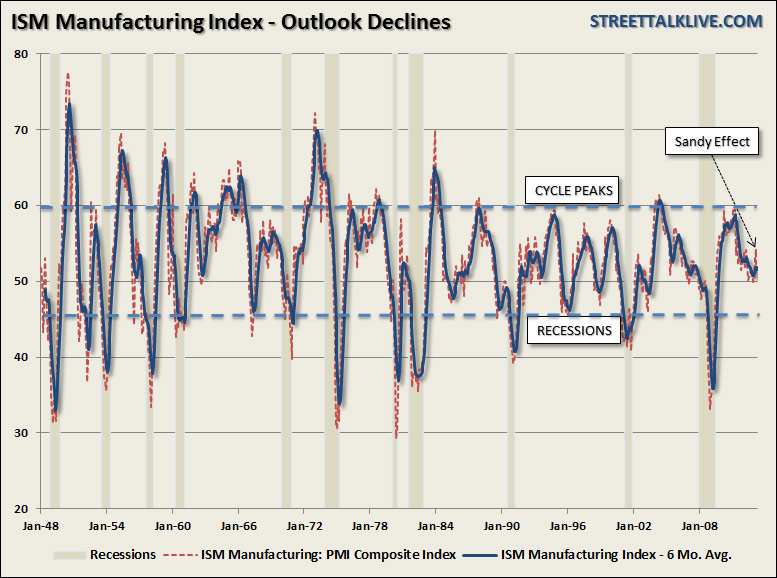

ISM Manufacturing Survey

The April Institute of Supply Management manufacturing survey added another ding to the mainstream’s economic “growth” story as it fell to near contraction territory coming in at 50.7 for April down from 51.3 in March. After a bump in the survey due to the economic boost provided by “Hurricane Sandy” – the trend of overall weakness has resumed. As with the majority of other economic reports recently – the ISM survey peaked 2011 and has been on the decline since.

Chicago PMI

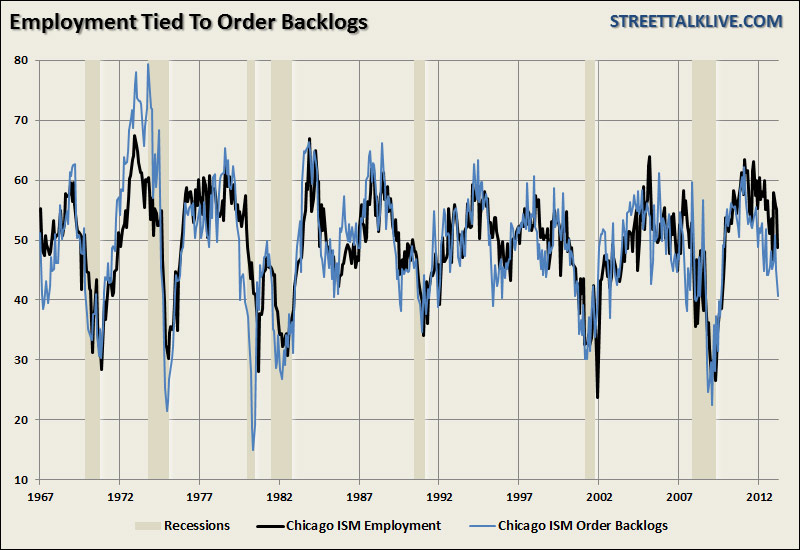

Following onto the ISM manufacturing survey was the Chicago Purchasing Managers Index (PMI). As opposed to the ISM report which had a few positives, such as strength in new orders and backlogs, there were no silver linings to be had within the PMI report.

For the month of April the overall index plunged from 52.4 in March to 49 in April which is a sign of economic contraction. Within the details of the report there was significant weakness.

Employment fell to 48.7 from 55.1 in March. This is not surprising when looking at the order backlogs which plunged from 50.9 in February to 45 in March and 40.6 in April. The decline in backlog orders means there is little need to increase employment. The chart below shows the correlation between backlogs and employment.

Production, inventories, supplier deliveries, and pricing pressure also showed signs of significant slack in the overall supply chain.

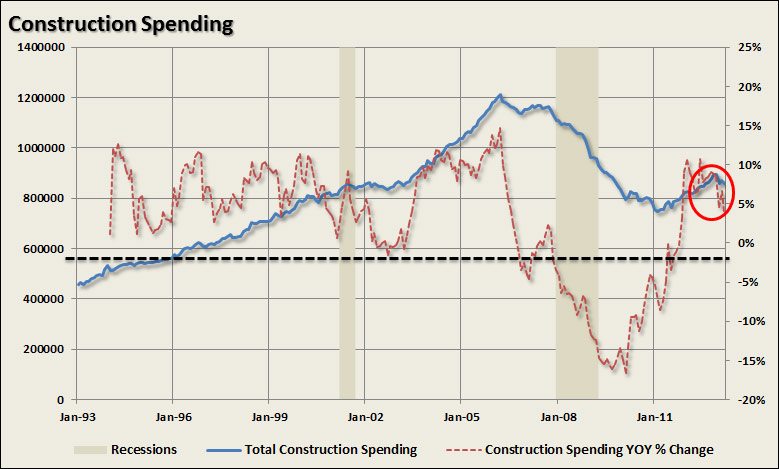

Construction Spending

The “housing and economic recovery” story may be running out of steam sooner rather than later. After recovering slightly in February from the near 4% plunge in January – construction spending plunged again in March falling 1.67% or .5 billion. One of the biggest economic multipliers is construction and its related spending. The decline is construction spending is troublesome to say the least for the economic "bulls".

Of course, the recent increase in the rate of economic deterioration has been completely ignored by the financial markets which have pushed toward new highs. Of course, this may be more of a function of “bad news means more QE” so “buy stocks.” The problem with this view is that the widening spread between rising prices and deteriorating fundamentals increases the magnitude of a future mean reversion.

That reversion becomes especially dangerous when a near record level in leverage, as measured by margin debt, is factored into the equation. Despite the Fed’s assertion that they have the capability to withdraw stimulative measures before an asset bubble is formed…past history shows this as a very unlikely possibility.

As investors it is critically important to be aware of the rising risks in the markets. History tells us that reversions are swift and brutal things that give individuals little warning with which to protect investment capital. There is no doubt that the markets can continue to be elevated given the massive liquidity measures that have been undertaken by global central banks. However, being lulled into complacency by the belief that such a situation will be indefinitely sustainable is likely to have very negative consequences.

Source: Street Talk Live