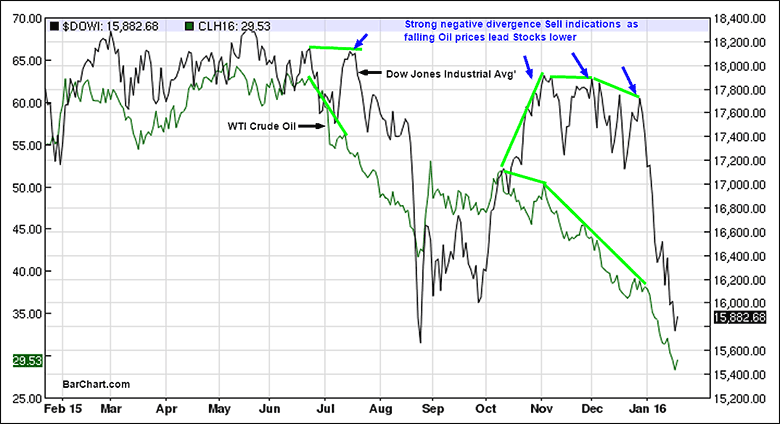

Since North American petroleum production spawned an oil bear market in 2014, energy prices have had a commanding influence on stock prices. As US stock prices repeatedly retested their previous highs last July and again in late December 2015, we witnessed an extreme negative divergence with oil prices signaling trouble for equities. Each time oil fell to new lows the Dow could not resist the rising perception of global slowing and eventually crashed over 10% each time. If soothsayers can determine when oil will bottom, we can be assured that stocks will follow suit.

Pessimism Peaks

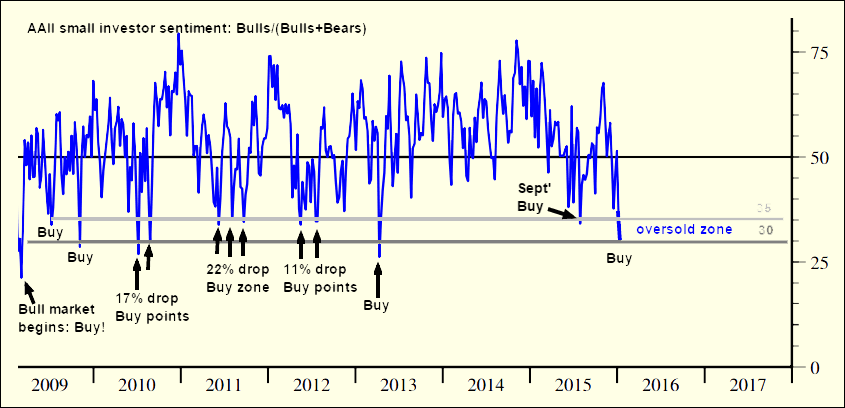

The American Association of Individual Investors (AAII) measures the sentiment of its members. Historically, stock market corrections are about over and its a good time to begin buying when member Bulls reach the current level of 18% and the Bulls/(Bulls+Bears) reach this week's 30% reading. While the global slowing theme has not been altered and the earnings valuation trend is flat, we have to look at dips for Buying once again as our minimum correction levels have been achieved at a time when negative sentiment has consistently signaled a low risk bottom being formed when at current extreme levels.

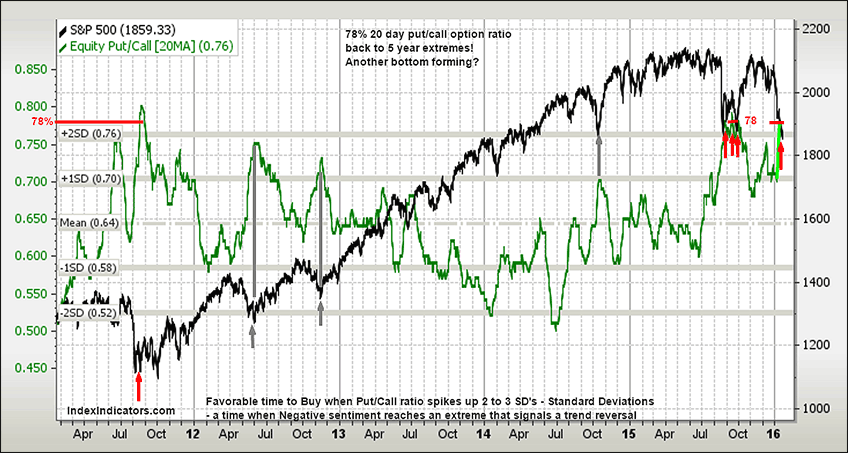

There are many sentiment measures screaming the same thing—that a stock market trough is near. The action by the 20-day moving average of put to call options is also at historic levels of pessimism where traders buy puts on stocks and indices betting prices will fall short term. While the current 78% ratio is rare and very accurate as a short term predictor to begin buying, we also like looking at general 2 to 3 standard deviation (SD) moves in the Put/Call ratio as a signal that an important inflection point is close at hand. Both requirements have been met which is why we expected that the mid 15,000’s on the Dow Jones Industrial Average (Dow) and 1800 area on the S&P 500 Index would mark the start of a bottoming formation for lower risk reinvesting of capital.

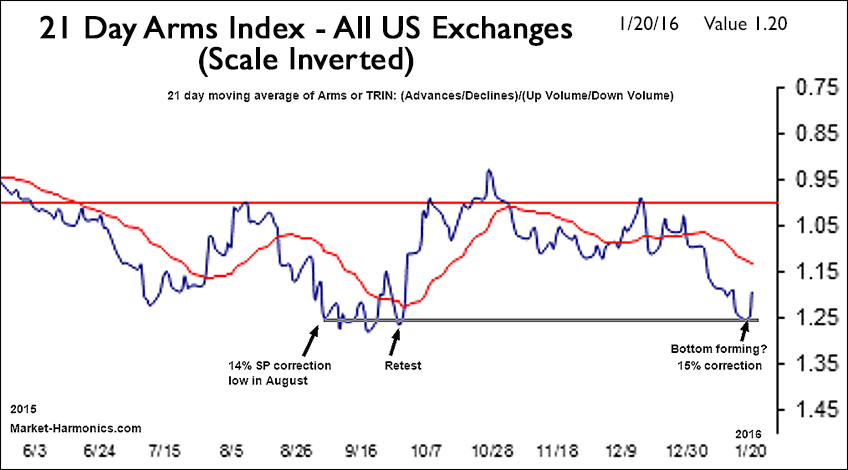

Most momentum indicators such as the Advance Decline line, high low ratios and others understandably can’t generate buy signals with the initial thrust down in January until there is a retest of stock market lows during a bottoming formation. This phase has likely just begun. However, we will conclude our technical case for a low with a breadth indicator of the TRIN or Arms Index which measures the Advancing stocks divided by decliners which is then divided by the total of their up volume divided by down volume. At the major 14% correction lows last August and in September the 21 day moving average of Arms hit significant oversold levels at or below 1.25. As prices spiked to their lows this week at Dow 15,450, 15% off the 2015 record highs, Arms again fell to 1.25 indicating an extreme oversold condition was forming over the near term.

Conclusion

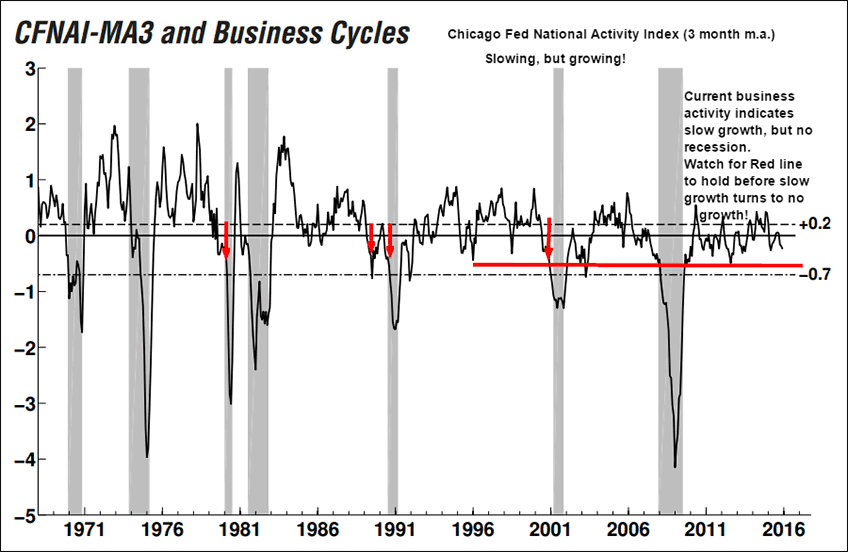

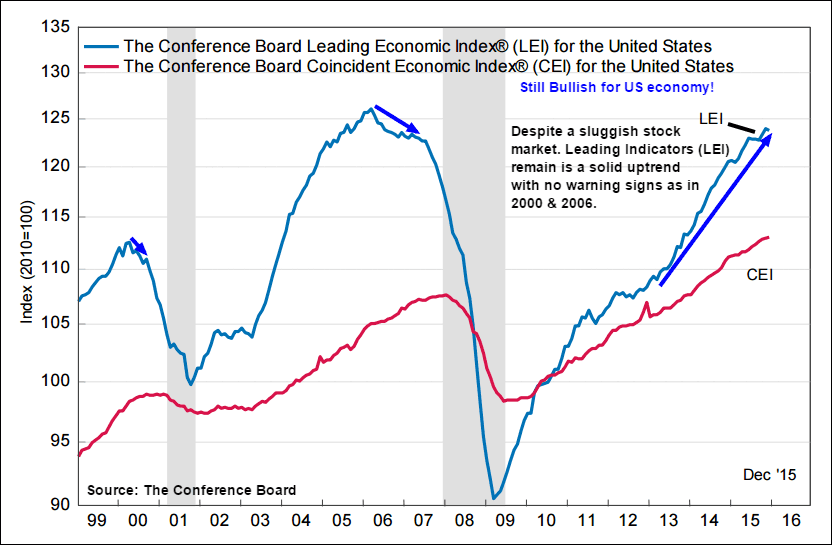

There is no fundamental reason for stocks, earnings and the world economy to accelerate in the near term and technically there has been significant damage to US and world stock indices. However, other than a flash crash aberration from further deflation in oil prices and junk bonds catalyzed by further slowing in China, there is also no reason to expect an outright recession yet as long as the National Activity Index and Leading Indicators (below) are holding above key negative thresholds.

Add to these stable fundamental measures the confluence of oversold technical indications highlighted earlier which leads us to favor that an initial momentum low in stock prices has arrived and that a bottoming formation is the most likely outcome over the next 3 to 6 weeks. A mid-February to early March stock market retest could be at a higher low or slightly lower low, but increasing exposure to stocks is warranted for now at or below the 15,700 Dow and 1835 S&P 500 Index levels which were just achieved. With Oil rallying over a barrel from its spike low this week beneath we all should stay tuned for the inevitable pullback phase in oil soon that will weaken stocks once again. Oil under will send stocks back to their lows and risk a new leg down assuming oil prices are consistently hitting new lows as well. This is a year where investors would be prudent to await corrections, such as this 15% drop, before increasing their stock market exposure.