In a presentation to Michigan Tech finance students and local executives Narayana Kocherlakota, President of the Federal Reserve Bank of Minneapolis, last month discussed the use of monetary policy to address labor market issues arising from the Great Recession of 2008 (picture at right courtesy Michigan Tech School of Business and Economics).

In a presentation to Michigan Tech finance students and local executives Narayana Kocherlakota, President of the Federal Reserve Bank of Minneapolis, last month discussed the use of monetary policy to address labor market issues arising from the Great Recession of 2008 (picture at right courtesy Michigan Tech School of Business and Economics).

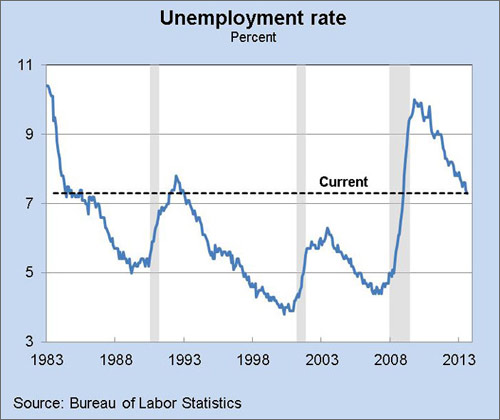

Kocherlakota began by documenting “the disturbing state of the labor market” noting the unemployment rate was 4.4 percent in March of 2007 and slowly rose to reach 5.0 percent by the end of the year. The National Bureau of Economic Research dates the Great Recession as having begun at the start of 2008, with the unemployment rate reaching a peak of 10 percent in October 2009 (see charts below).

[Hear More: Rick Santelli: Labor Force Participation Rate Lowest Since 1978]

Kocherlakota claims that “this measure—troubling as it is—overstates the improvement in the U.S. labor market.” He continues:

“This characterization is borne out if we look at the evolution of the fraction of people over the age of 16 who have a job—what’s called the employment-to-population ratio. In March 2007, the employment-to-population ratio was over 63 percent. The employment-to-population ratio fell sharply during the Great Recession and bottomed out at just over 58 percent in mid-2011. The percentage has risen little from this low point and remains lower than at any time between 1986 and 2007.

To summarize what we learn from the charts: The good news is that the labor market has improved since the end of the Great Recession. The bad news is that the rate of improvement over the past four years has been painfully slow. As a consequence, the condition of the labor market remains weak.”

With labor markets weak Kocherlakota pointed out that inflation is also very subdued, which opens the door for the use of additional monetary tools:

“I have shown you evidence that the labor market is currently weak. But the charts also show that the labor market has been weak for several years. Some observers have concluded from this persistence that monetary policy cannot ameliorate the problems in the labor market. One of my main points today is that this conclusion of monetary policy impotence is at odds with the behavior of inflation.

To understand this point, it’s useful to look at the behavior of personal consumption expenditure (PCE) inflation over the past few years. Just to be clear, this is a measure of inflation that incorporates the prices of all goods and services, including food and energy. Since the beginning of the Great Recession in December 2007, the PCE inflation rate has averaged around 1.5 percent. This is noticeably below the FOMC’s target inflation rate of 2 percent per year. And the outlook for future inflation is similarly subdued. Thus, earlier this year, the Congressional Budget Office projected that PCE inflation will remain below the FOMC’s target of 2 percent until the year 2018. These low levels of inflation tell us that monetary policy can be useful in increasing the rate of improvement in the labor market…”

Kocherlakota concludes that the Fed “faces a challenging macroeconomic problem—although this time, the problem is stubbornly low employment as opposed to stubbornly high inflation.” He claims that monetary policy can address this problem, and that the Fed should continue to use “unconventional monetary policy tools” like those employed in the past few years.

“Doing whatever it takes will mean keeping a historically unusual amount of monetary stimulus in place” he notes, “and possibly providing more stimulus—even as:

- Interest rates remain near historic lows.

- Economic grow rises above historical averages.

- Per capita employment begins to rise appreciably.

- Asset prices rise to unusually high levels, leading to concerns about ‘bubbles.’

- The medium-term inflation outlook rises temporarily above 2 percent.”

He made two recommendations: (1) The Fed should communicate that “their goal is to accomplish a return to maximal employment while keeping inflation close to, although possibly temporarily above, the target of 2 percent”, and (2) to do “whatever it takes, on an ongoing basis, to achieve that goal”.

While Dr. Kocherlakota’s view is only one voice of the Federal Reserve, his status as President of the Federal Reserve Bank of Minneapolis adds weight to his commentary and analysis.

Should the Fed continue to provide liquidity to the global economy the investment implications for equity investors is positive. As he notes asset prices might rise to ‘unusually high levels’. Academic studies have indicated that equity markets tend to perform very well during periods of easy monetary policy.

Note: A copy of Dr. Kocherlakota’s presentation can be found on the Minneapolis Federal Reserve website.