The recent cuts in Chinese interest rates underline the economic headaches that China is facing. Between long-term reforms and short-term weakening, there appears to be no easy solution for China’s monetary policy.

As China embarked on a comprehensive long-term reform program aimed at rebalancing its economy from one driven by exports and investment to a more sustainable consumer-based model, the short-term pressures are increasing.

After months of downward revisions to growth forecasts, the Chinese slowdown is now officially admitted with Premier Li Keqiang announcing the government target for GDP growth to be down to 7%.

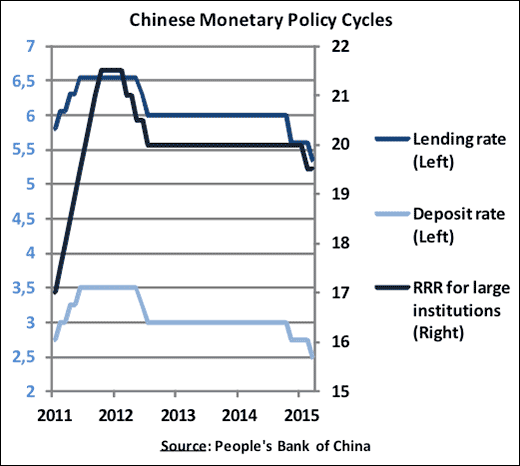

Because the series of targeted measures last year (different requirements depending on the sector and type of financial institution) have not displayed significant results, the People’s Bank of China (PBoC) is now moving to broader and more traditional monetary policy.

Having resisted the pressure for two years, the PBoC started the relaxation with a first cut in the benchmark interest rates (lending and deposit) in November 2014, and followed this month by a second cut.

Furthermore, the reserve requirement ratio for large institutions was also cut so that liquidity can be released in the system. The Renminbi (RMB) is starting to fall. The monetary policy cycle is in the ease mode. Why and why not more?

Short-Term Reasons to Cut and Let the RMB Fall

There are indeed plenty of apparent reasons why monetary policy should be eased, not the least to give some relief from downward pressures on growth and domestic prices.

1. An appreciating currency harms exports:

The world is currently in a state of raging currency wars from the major advanced economies. The U.S., U.K., Eurozone and Japan have all embarked in quantitative easing in part with the aim of depreciating their currency and favoring their exports.

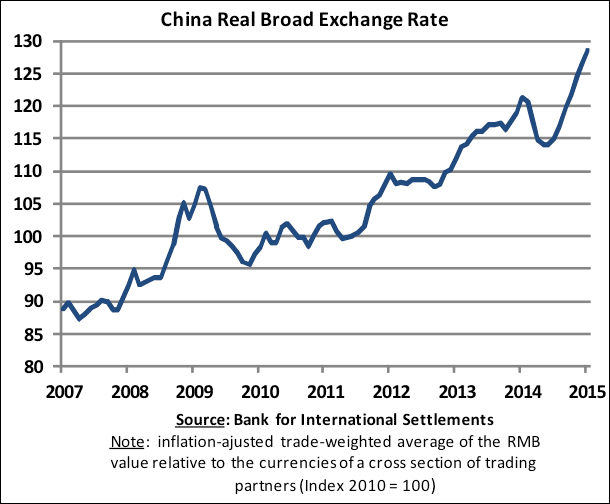

This has been a hard hit for the Chinese currency, which appreciated sharply – 31% over the past five years relatively to its main trading partners:

At the same time as the U.S. Congress was continuing debates about China’s alleged currency manipulation, Chinese exports have actually suffered dramatically. In an economy where exports account for a quarter of its GDP, the consequences for growth are very real.

But an appreciating currency also makes China’s import much cheaper, in turn pushing domestic prices downward.

2. The deflation risk

Thus, as the advanced economies and newspapers’ headlines are all about deflation, China is also having its own low inflation problem. The latest available data points to an inflation rate at 0.8% year-on-year in January, giving ground for further monetary easing.

All in all, facing a sharp currency appreciation against most of China’s trading partners, facing downward pressures on domestic prices, with decreasing fixed asset investment (FAI) and slowing growth, it seems reasonable and straightforward for the monetary policy to be relaxed.

Long-Term Reasons Not to Cut and Resist a RMB Fall

This, however, runs against the structural reforms that China has started. Hence the recurrent and well-known trade-off: short-term pain for long-term gain?

1. A further increase in instability and a hit for the rebalancing process

For the past two years, PBoC president Zhou Xiaochuan and the government have resisted expansionary monetary policy and big growth-sustaining stimulus programs exactly for this reason. And it worked.

The indicators of such a rebalancing seem broadly positive: disposable income of households has been growing faster than GDP and housing investment growth has trended down, while loans to SMEs are growing faster than loans to big enterprises.

Hence, although it is true that in China one needs to look beyond the interest rates to analyze credit growth, it is reasonable to worry that rate cuts reignite the borrowing binge that led to overheating and dramatic debt levels – which is also exactly what the government is fighting. The November 2014 rate cut had indeed fueled a speculative boom in the stock market.

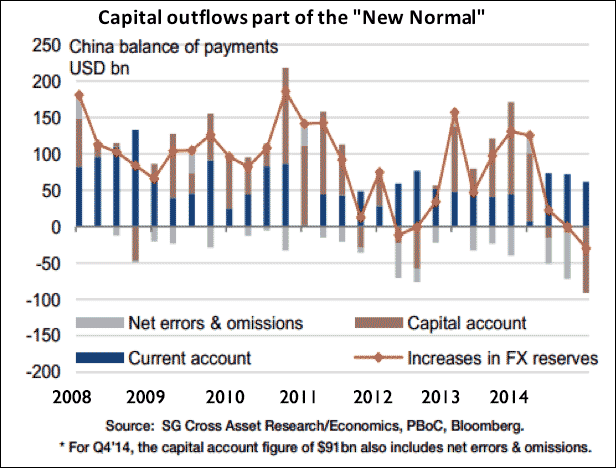

2. Aggravating capital flight

For years, China has experienced massive capital inflows, following a strategy of “carry trade”: borrowing short-term from U.S. or European banks at very low interest rates and investing this money in China where the RMB return was much higher – hence benefiting from the interest rate differential.

These huge flows coming in were sterilized by the PBoC, notably through increase in the reserve requirements of banks (see first chart). By contrast, in recent months China has faced important capital outflows as the carry trade story unwinds: the expected rate hike from the U.S. Fed in mid-2015 will increase U.S. borrowing costs and Chinese rate cuts will diminish the RMB returns.

Capital account deficits are in fact becoming the new normal, leading to a consequent fall in FX reserves:

Thus, capital flight should further increase as Chinese monetary policy gets more accommodative.

3. Increasing tensions with international partners

The prospect of China joining the global currency war is indeed a worrying perspective if competitive currency devaluation imposes itself one more time as conventional financial weapon.

On the trading side, China-bashing will be revived by the main trading partners. The recent move by Barack Obama against China at the WTO regarding “common service platforms” is a case in point.

China Navigates Between Challenges

For many, these timid rate cuts have clearly not done enough to fight the slowdown and deflation risk. Hence, there seems to be a consensus among economists that at least one further cut in the benchmark rate and one cut in the RRR ratio will happen before the summer.

At the same time, the PBoC is painfully trying to keep its narrative that those cuts are not “easing”, or “change in monetary policy direction” but a prudent and “neutral operation of timely and appropriate fine tuning” to adjust the economic structure.

We can indeed hope with Stephen S. Roach that “strategy is China’s greatest strength. Time and again, Chinese officials have successfully coped with unexpected developments, without losing sight of their long-term strategic objectives.”

But once again, for monetary and exchange rate policy as for any other branch of its policymaking, China will have to force itself an uncertain path between its conflicting goals.

Related:

Inverted Balance Sheets and Doubling the Financial Bet